This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Automotive OEMs that successfully integrate carbon net-zero strategies across their value chains will not only achieve regulatory compliance but also secure strategic leadership in a decarbonized global economy. By Thanigesh Arumugam Parthasarathi, Team Leader Mobility Carbon neutrality has become a key priority for global automotive OEMs.

The Australian automotive aftermarket, now in a mature phase, is on a trajectory for significant growth through 2030. The increase in total vehicles in operation (VIOs), coupled with the increasing proportion of aging vehicles, is set to generate robust demand for automotive parts and services. from 2023 to 2030.

By Gautham Hegde, Senior Research Analyst – Mobility As technological advancements reshape the automotive landscape, consumer preferences for greater connectivity, convenience, personalization, and flexibility are driving significant growth in Feature on Demand (FoD) services.

One such beneficiary is automotive audio technology – basic audio, surround sound, and 3D audio – which, in North America alone, is set to grow from a $3.33 billion in 2030. Growth in the automotive audio market is being propelled by connectivity trends that are supporting continuously improving in-vehicle audio entertainment.

As the automotive industry evolves, so is the need for advanced diagnostic solutions that keep pace with increasingly complex vehicles. Diagnostics-as-a-Service (DaaS) has emerged as a groundbreaking business model offering significant benefits for automotive workshops, dealerships, and collision centers worldwide. billion by 2030.

Leading Asian automakers like BYD, Nio, Toyota, Honda, and Hyundai look to partnerships, platforms, and new business models to align with evolving software-driven automotive industry. As SDV strategies evolve, automotive original equipment manufacturers (OEMs) are shifting their architectural and developmental approaches.

By Benson Augustine, Program Manager – Mobility The global automotive aftermarket is witnessing a paradigm shift as circular economy initiatives gain momentum. Revenues of the global remanufactured automotive components market are projected to rise from $27 billion in 2022 to $42 billion by 2030.

Electromobility is gaining momentum with improving charging infrastructure, expanding manufacturing capacity, policy support, and purchase incentives. million by 2030, with all major automakers aggressively expanding their EV portfolios in the quest for zero emissions. A Booming eMobility Aftermarket is Expected Emerge by 2030.

Overall sales across 10 Caribbean and Central American automotive markets set to surpass 300,000 units by 2030, with battery electric vehicles (BEVs) doubling their share from current levels. At the same time, the shift toward digital retailing and online dealerships is transforming how consumers interact with automotive brands.

By Benson Augustine, Senior Industry Analyst, Aftermarket & Digital Retail – Mobility Rematec, a leading trade show for stakeholders in the automotive remanufacturing ecosystem, was held in Amsterdam in June this year, after a four-year hiatus. North America and Europe currently dominate the global reman aftermarket.

Conventional engine, transmission, and affiliated components will represent immediate high-growth opportunities in the automotive aftermarket, while the transition to vehicle electrification will drive investments in electric vehicle (EV) related remanufacturing.

With the EU committed to more than halving its GHG emissions by 2030, it has become imperative for automakers to balance revenues with regulatory compliance, and economics with environmental considerations. In order to pursue this objective, there are plans to operate about 6 battery giga factories in Europe by 2030. 3 GTX, and the ID.2

Data security and privacy remain major concerns as automakers move to embrace ChatGPT across the automotive value chain. Generative AI-powered Large Language Models (LLM), most prominently ChatGPT, are disrupting the automotive industry. Where will it be used? We see four key areas where ChatGPT will have an immediate impact.

Chinese Tier 1 automotive suppliers have emerged as pivotal players in the rapidly transforming global automotive market, leveraging their technological capabilities and innovation to capture significant global market share. Strategic partnerships with established global players are another significant growth driver.

Market Landscape in 2023 For a variety of reasons ranging from supply chain disruptions to macroeconomic headwinds, passenger vehicle and pickup vehicle sales across the five main automotive markets of Indonesia, Malaysia, the Philippines, Thailand, and Vietnam dipped from 3.2 million in 2022 to 3.1 million units in 2023.

Synergies between automotive OEMs and battery manufacturers to ramp up collaborative initiatives in battery development. As battery manufacturers look to scale up their manufacturing capability, the spotlight is on gigafactories. CAGR over 2022-2030. EV sales are estimated to increase from 10.5

The eCommerce boom, digital platforms, and mobile on-demand services are transforming the automotive aftermarket across the Gulf Cooperation Council (GCC) region. The absence of a robust local manufacturing base for automotive components has made the region extremely import dependent. billion in 2028.

Sustainability is at the heart of disruptive transformation across the automotive industry. Beyond OEMs, tire manufacturers are also playing a key role in the transition. Leading tire manufacturer Bridgestone has developed specialized EV tires – the Alenza – for BMW’s all-electric iX.

This convergence of automotive, technology, and entertainment is pushing the evolution of larger, more sophisticated in-car displays. billion by 2030, highlighting its substantial growth potential. Frost & Sullivan projects the European in-vehicle display market to reach $5.76

This convergence of automotive, technology, and entertainment is pushing the evolution of larger, more sophisticated in-car displays. billion by 2030, highlighting its substantial growth potential. Frost & Sullivan projects the European in-vehicle display market to reach $5.76

This convergence of automotive, technology, and entertainment is pushing the evolution of larger, more sophisticated in-car displays. billion by 2030, highlighting its substantial growth potential. Frost & Sullivan projects the European in-vehicle display market to reach $5.76

Powertrain diversification, connected cars, and new mobility models will further impact market dynamics By Ingrid Schumann, Industry Analyst – Mobility In March this year, leading automaker Stellantis announced the “largest investment in the history of the Brazilian and South American automotive industry.”

However, the announcement in April earlier this year that US luxury EV manufacturer, the Lucid Group, will be delivering 100,000 EVs over a ten-year period as part of a deal struck with the Government of Saudi Arabia underscores the country’s commitment to transitioning to more environmentally friendly, zero-emissions transport.

To learn more, please access our research reports, Global Shared Mobility Outlook, 2022 and Global Autonomous Shared Mobility Growth Opportunities , or contact sathyanarayanak@frost.com for information on a private briefing. trillion by 2030. billion (Rs 22,400 crore) in revenue by 2030. A Unique Marketplace Solution.

Both government and the automotive industry have established hydrogen roadmaps, even as they focus on overcoming challenges related to high production and maintenance costs, nascent supply chains, as well as inadequate refueling infrastructure. The buzz is getting louder as vehicle manufacturers start expanding their FCEV portfolios.

The recent partnership between German auto giant, BMW, and leading cloud computing solutions provider Amazon Web Services (AWS) underlines the critical need for effectively handling, processing, managing, and protecting vehicle data at a time when the automotive ecosystem is being transformed by C.A.S.E. Our Perspective.

Therefore, while silicon semiconductors will continue to dominate for the next three to four years, Frost & Sullivan projects that they will be overtaken by SiC and GaN semiconductors over 2027 to 2030. Simultaneously, advances in material chemistry will be accompanied by innovations in design and manufacturing processes.

Leading US-based automotive supplier BorgWarner is amping up its electrification journey – encapsulated in the “Charging Forward” initiative – and its commitment to sustainable mobility solutions. In early December, the company announced its intention of cleaving its fuel systems and aftermarket segments into a separate, new entity.

More overarchingly, this shift towards truck electrification represents a first step to realizing Boliden’s commitment to lowering carbon emissions – much of which is related to diesel vehicle usage – by 40% by 2030. The use of Volvo’s trucks in Boliden’s mine will support a safer and more sustainable production environment.

million units by 2030. To learn more, please access: Growth Opportunities in China’s Electric Vehicle Industry, 2024-2030 , Strategic Profile of BYD , ASEAN Automotive Market Outlook, 2024 , or contact sathyanarayanak@frost.com for information on a private briefing. million units in 2023 to an estimated 25.2

million mark in 2022 and are expected to comprise more than 50% of new vehicle production by 2030 – the Japanese automaker announced that it would target annual sales of 1.5 Our Perspective The EV segment was the bright spark in a relatively dull global automotive market in 2022. million BEVs, globally, by 2030.

Surging investments target 200,000 fuel cell electric vehicle (FCEV) units by 2030. Stakeholder collaboration between governments, automotive companies and other ecosystem participants is further accelerating passenger FCEV uptake. of global sales by 2030. of global sales by 2030. In 2022, Hyundai Motor declared a $6.7

Turns out Volkswagen’s infamous “Dieselgate” was not deterrent enough, and Fiat Chrysler Automobiles (FCA) has become the latest automotive company to be indicted for attempting to cheat its way past emissions testing regulations. Major Trends in Passenger Car OEM Strategies for CO 2 Emissions Compliance. reduction from 2020 levels.

This year’s CES 2023 shone the spotlight on two key trends in the automotive industry: electrification and digital transformation. Several Chinese automotive companies like Nio, Li Auto, and XPeng have been at the cutting-edge of this convergence, combining advanced connectivity and autonomous technologies with vehicle electrification.

These include plans for ICVs with partial and conditional automation features to account for more than 70% of new vehicle sales, highly automated ICVs to account for more than 50% of new sales, and almost all new vehicles to be equipped with C-V2X capabilities by 2030. Autonomous technology itself is still in the early stages of development.

The US Department of Energy predicts a five to ten-fold increase in global electric vehicle (EV) battery demand by 2030. Accordingly, battery manufacturing companies are accelerating their focus on advanced new battery technologies that overcome the limitations of current offerings.

In addition to creating a more localized supply chain for the Indian market, this strategy also envisages India emerging as a manufacturing center for EV parts export to other Southeast Asian markets. The thrust is on increased localization and domestic manufacturing. Our Perspective.

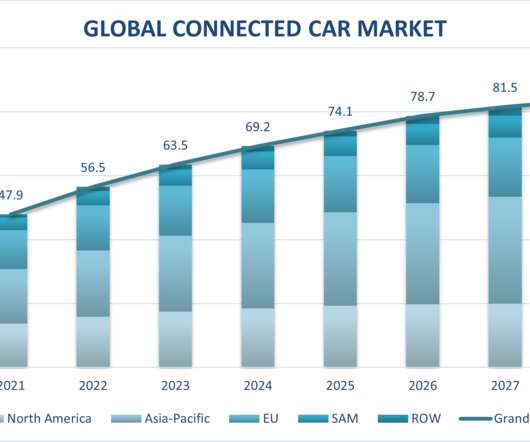

Strategic partnerships between telematics service providers (TSPs), original equipment manufacturers (OEMs), and other technology facilitators are delivering new value propositions for users. Established technologies, distribution networks, and supply chains will support steady growth until the end of 2030. million by the end of 2028.

Strategic partnerships between telematics service providers (TSPs), original equipment manufacturers (OEMs), and other technology facilitators are delivering new value propositions for users. Established technologies, distribution networks, and supply chains will support steady growth until the end of 2030. million by the end of 2028.

Strategic partnerships between telematics service providers (TSPs), original equipment manufacturers (OEMs), and other technology facilitators are delivering new value propositions for users. Established technologies, distribution networks, and supply chains will support steady growth until the end of 2030. million by the end of 2028.

Manufacturing and sales of these systems are set to start in 2023. According to the International Energy Agency, close to 250 million EVs will be on the world’s roads by 2030. As importantly, batteries that cannot be repurposed will be dispatched for recycling or reuse in other applications or will be safely disposed.

OEMs will continue to collaborate with various companies in the automotive value chain to expedite the development and implementation of hands-off and eyes-off technologies. Collaborations between OEMs, tier suppliers, and semiconductor manufacturers will focus on creating tailor-made integrated circuits (ICs) and software-on-chip (SoCs).

OEMs will continue to collaborate with various companies in the automotive value chain to expedite the development and implementation of hands-off and eyes-off technologies. Collaborations between OEMs, tier suppliers, and semiconductor manufacturers will focus on creating tailor-made integrated circuits (ICs) and software-on-chip (SoCs).

OEMs will continue to collaborate with various companies in the automotive value chain to expedite the development and implementation of hands-off and eyes-off technologies. Collaborations between OEMs, tier suppliers, and semiconductor manufacturers will focus on creating tailor-made integrated circuits (ICs) and software-on-chip (SoCs).

We organize all of the trending information in your field so you don't have to. Join 45,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content