Metalworking Activity Contracted Marginally in April

The GBI Metalworking Index in April looked a lot like March, contracting at a marginally greater degree.

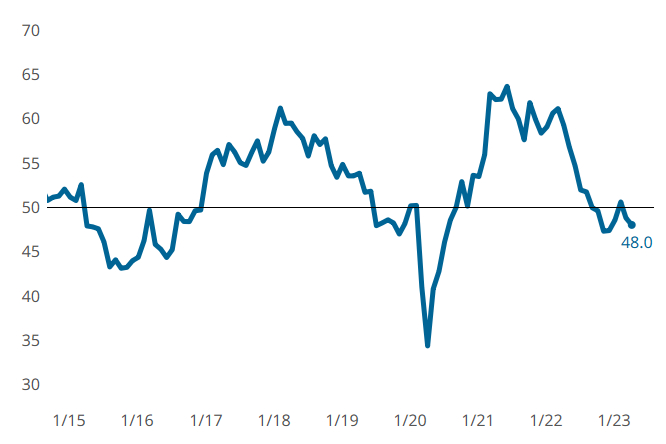

The Metalworking Index closed at 48.0 in April, down almost one point versus March. Similarly, components minimally strayed from March readings in April, with three of the six — new orders, exports and backlog — contracting at the same pace or a bit faster versus last month.

Production, which had crept into expansion in March, was flat in April. Supplier deliveries continued to lengthen more slowly and employment continued to expand more quickly in April. Both are potentially holdovers from Covid-inspired supply chain issues and labor shortages, respectively.

A separate but related non-GBI metric, future business, still expanded, but at a slower rate in April — in fact, at the slowest rate since July 2022. The brakes appear to have been put on metrics that just recently had been moving in ‘favorable’ directions, which is disappointing. At the same time, it is encouraging that the shift was not more dramatic.

Metalworking GBI in April looks a lot like March, contracting for a second month in a row. Photo Credit: Gardner Intelligence

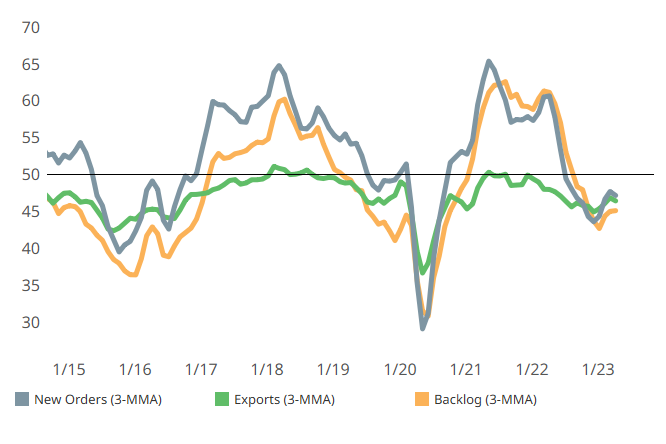

New orders, backlog and export activities contracted about the same in April as March. (3-MMA = three-month moving averages). Photo Credit: Gardner Intelligence

Related Content

-

Metalworking Growth Stays Consistent in August

All components of metalworking activity contributed to the consistent slowdown in the past few months.

-

Breaking News from 2021 World Machine Tool Survey

Move over, July GBI! Gardner Intelligence offers a special update on the World Machine Tool Survey in place of its typical Gardner Business Index column.

-

Metalworking Activity Stays Flat in October

The GBI for Metalworking reflects stability of most of the six GBI components that had been losing ground months prior. Ordinarily underwhelming, flat is good when it means not contracting.