Senior Editor

Steel mills start to show signs that they see demand softening for their products. pixelprof/E+

I sometimes think of Steel Market Update (SMU) as an early warning system for big market moves, and our most recent survey data clearly points to a market inflection.

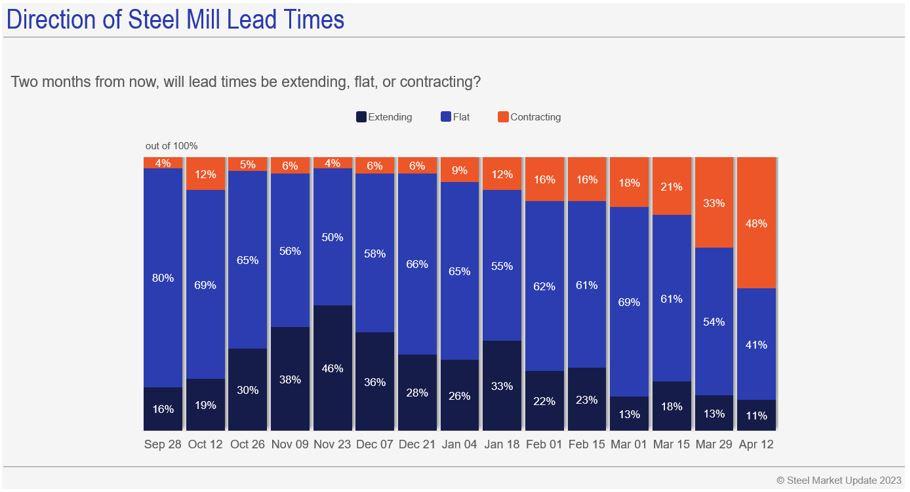

For starters, nearly half of respondents to our latest survey think lead times will be contracting two months from now. Figure 1 illustrates that shift in thinking.

There are some seasonal reasons for that—namely, the summer doldrums. Still, a shift in lead times often is a precursor to price moves.

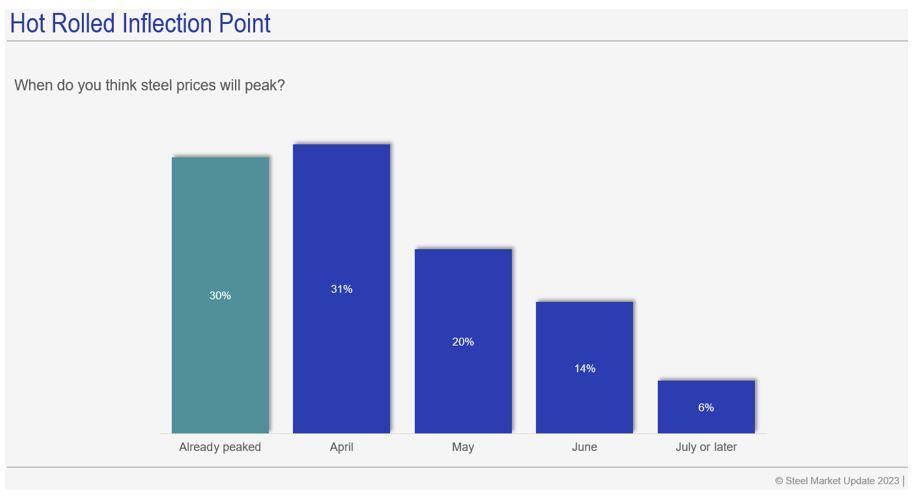

Also, more than 80% of survey respondents think that hot-rolled coil (HRC) prices have already peaked or will before Memorial Day (see Figure 2).

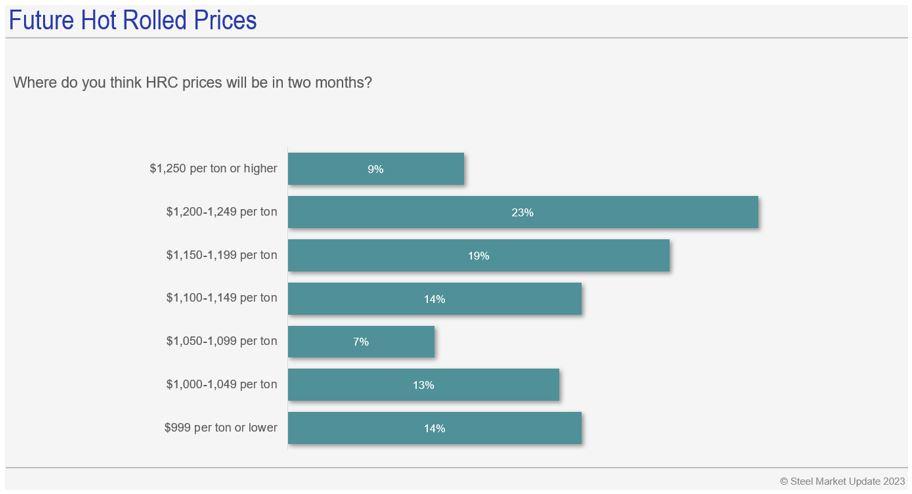

Finally, only 9% of respondents think HRC prices at or above $1,250/ton ($62.50/cwt) are in the cards (see Figure 3).

That’s notable because Cleveland-Cliffs announced that it was raising spot HRC prices to $1,300/ton in early April. Yet fewer steel buyers expect to see such a price point now. In an SMU survey before this most recent one, 20% thought an HRC price of more than $1,250/ton was likely.

It’s not like these results are occurring in a vacuum. We’ve seen a host of important indicators change direction this month.

Our future sentiment readings remain below current sentiment. That’s sort of our version of an inverted yield curve.

Scrap prices fell in April for the first time since December, and metallics prices are expected to trend downward in May as well. It’s not unusual to see that happen this time of year, but it’s one less reason for mills to hold on to current high prices.

Finally, lead times, which stopped extending in the second half of March, have fallen significantly for the first time since late November. The dip in lead times comes as mills are more willing to negotiate spot prices, another big trend change.

Figure 1. Steel buyers increasingly have the sense that demand for steel will be declining, leading to contracting lead times from the mills.

That’s the data. So what are people saying? The anecdotes I’ve gleaned are mostly in sync with our survey results.

A Midwest service center source, for example, told me a northern mill was offering $1,100/ton or less for larger orders (think thousands of tons). That was at least $60/ton below our published HRC price at the time ($1,160/ton).

The absolute numbers there matter less than the trend. When the market is moving upward, we typically hear that offer prices are higher than our latest published price. (We update our prices every Tuesday evening.) When the market is falling, the reverse is true.

Another example: A service center executive in the Ohio Valley told me that a domestic mill had reduced his base price for galvanized product by about $30/ton since we last spoke. That might not be worth noting at another point in the cycle, but it is notable now because he’d seen almost nothing but increasing prices since late last year.

Some wild cards are out there, however, and people should keep an eye out for them. We’ve reported in a prior issue about lengthy unplanned outages at ArcelorMittal’s blast furnaces in Europe. I thought I might be writing this week that things were tighter than expected because of that.

Recall that unanticipated production problems at Mexican flat-rolled steelmaker AHMSA were among the catalysts for sharply higher prices in the first quarter. Maybe the reduction in European supply will have an effect in the U.S. But to date, I’m not hearing much.

Are some people having trouble finding certain niche items that they might have bought from ArcelorMittal Europe? Yes. Are they having trouble getting enough steel in general? No.

In short, we’ve seen just about everything flattening out and trending lower. The only thing that hasn’t yet is price.

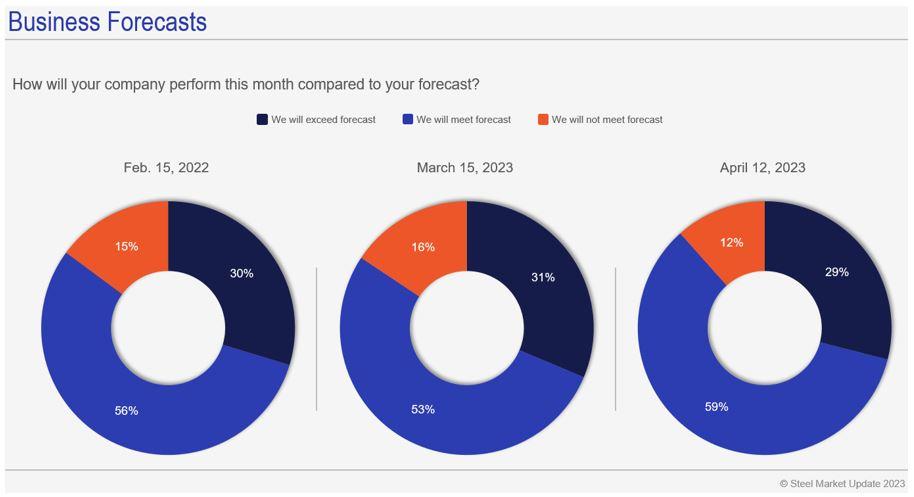

That said, it’s important not to get complacent about the market falling. I say that because most survey respondents continue to report that they are meeting or exceeding forecast (see Figure 4).

It could be that the 6% who think prices won’t peak until the second half of 2023 are onto something. Maybe they’re betting on fears of a price collapse extending the cycle? We’ve seen that happen before.

Figure 2. A vast majority of survey respondents believe that steel prices will peak by the end of May.

It also could be that they’re invested in higher prices. We’ve seen that in the past as well.

Mills have charged sharply higher prices throughout the first quarter. Many of their customers accepted those high prices, and so the last thing they want is to see them fall quickly, taking inventory values down along with them.

In short, we can see why prices might fall. Saying exactly when that might happen is always tricky.

If you find this data helpful, please play a part in bringing it together. See your company’s experience reflected in it! Contact us if you’d like to participate in our steel market survey at info@steelmarketupdate.com.

Registrations are already rolling in for SMU Steel Summit, our flagship event and the largest flat-rolled steel conference in North America. You can learn more and book your spot here.

The Steel Summit is Aug. 21-23 at the Georgia International Convention Center in Atlanta. We had nearly 1,300 people attend the event last year. We expect at least that many again this year.

Keynote speakers this year will include Cleveland-Cliffs Chairman/President/CEO Lourenco Goncalves; ITR Economics President Alan Beaulieu; and Barry Zekelman, executive chairman and CEO of Zekelman Industries. You won’t want to miss it!

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}